300 YEARS AGO, when the British Empire was still growing, the first wave of global trade was powered not only by the Pound Sterling, but by trades in Bills of Exchange.

How did traders from London buy tea in India, porcelain in Hong Kong, or silks in Singapore? They didn’t haul cases of silver and gold in their outbound ships, trading coins for goods. They had to do that when global trade began 500 years ago, but at the peak of the British Empire they bought goods with pieces of paper, specifically Bills of Exchange.

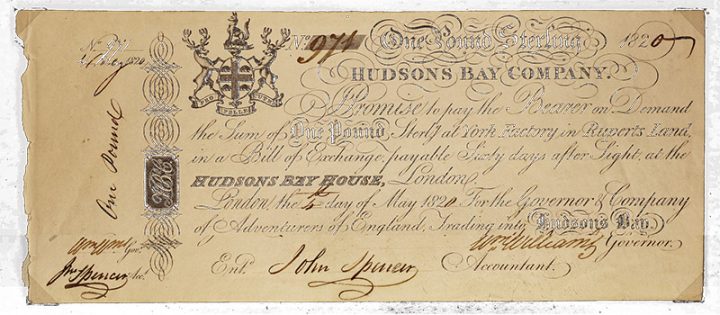

A Bill of Exchange is a fancy, formalized IOU. It is a promise to pay a specific amount on for before a specific future date. In modern terms, a Bill of Exchange is similar to a post-dated check, redeemable 90 days from the day it is signed. But this old-fashion IOU comes with one extra important feature that a post-dated check does not have. A Bill of Exchange is a tradable asset.

Remember, this story is from hundreds of years ago. Before the telegraph. Back in the days when communication was no faster than a ship could sail. Bank checks existed then, but the process of clearing those checks was far from overnight. Today it may take a day or two for a check to clear. Back then it could take months, as the actual paper check had to make its way to the bank where the check was issued in order to be traded for silver, gold, or simply for its value to be deposited in the recipient’s bank account.

Thus, was invented the Bill of Exchange. Or more specifically, reinvented, as the Chinese were using something similar hundreds of years before the British, and something similar was used by the banks of Renaissance Europe too, just not at the scale of the British Empire.

Discounts

What made these bills of exchange even more useful was the ability of banks (and other speculators) to buy Bills of Exchange at a discount, and then later, after passing through a few hands, exchange that Bill of Exchange in London for its full face value.

For example, an American tea trader in 1820 might send a ship to Bombay (now Mumbai) to buy a shipload of tea. The ship captain could pay for the tea by writing a Bill of Exchange, maturing in 90 days, using a letter of credit from Barclays Bank. The ship leaves full of tea, with 90 days to return home and sell the tea before any pounds are removed from the trader’s bank account in London (London being the center of global finance in the 1800s, not New York City).

Meanwhile, the tea seller has tea farmers and other bills to pay. So rather than putting the Bill of Exchange on another ship bound for London, waiting for the 90 days to expire, and then the Pound Sterling to arrive in Bombay (plus all the risk associated with that journey), the seller instead walks the yet-mature Bill of Exchange into a local Indian bank. That bank buys it for cash, at a discount to its face value.

The size of the discount is based on the creditworthiness of the trader, the prestige of the trader’s bank, and the distance between the local bank and London. That Bill of Exchange may get sold a few more times before it finally finds its way back to London, back to Barclays Bank, where it is finally redeemed at face value.

For example, the local Bombay bank might pay 94 pounds for the face value 100 pounds written on the Bill, as that buyer does business with a variety of London banks. A month later that Bill makes its way to Mombasa, Kenya where the local Barclays’ branch pays 98 pounds, as their risk is just transporting the Bill back to London where the main branch finally credits the full 100 pounds of value.

This system may feel complicated, but it worked for centuries. This was one of the unsung benefits created by the British Empire, empowering the growth of global commerce by both eliminating the need to transport heavy silver and gold around the world, as well as by creating a securitized form of credit that enabled sellers to be paid sooner than the 90 days it appeared they had to wait. That, and also remember that we take our near instant communications for granted today.

Less than twenty five years ago, at the end of the 20th Century, paper checks in every country were still being settled by flying the physical pieces of paper to one central city, sorting the paper checks by bank, and netting out the balances from bank to bank. It is only in the 21st Century when international bank wires and other international financial transactions are settled within minutes or hours, rather than in weeks or months.

RIP

In the handover of the mid-20th Century between the British Empire and American Hegemony, these Bills of Exchange were lost, replaced with international wire transfers and purchase orders.

Perhaps for the largest companies, that was an improvement. But for the smaller companies, it was a huge loss. Here in the early 21st Century, the most common form of agreement for not just global trade but also domestic commerce is a purchase order. Big customers order products from vendors, and more often than not, those big customers pay “Net 30” or “Net 45” or “Net 60”, i.e. they promise to pay the vendors 30, 45, or 60 days after delivery.

That gives the retailers time to sell the goods, earning the money to pay the vendors, or it gives the manufactures time to make and sell the products, earning the money to pay the vendors. But it leaves the vendor to finance that 30-60 day period, plus the 15-30 days before delivery when those vendors produced their products.

For small and medium sized companies, that simply isn’t fair and often simply isn’t possible.

I see this every week with my fledglings and bizi. They receive orders from big customers, but can’t fill those orders as they can’t pay their vendors in cash now and wait 45-90 days later to be paid. Banks don’t lend to small and medium businesses, even with a purchase order in hand from a big customer. Startup lenders, when they can be convinced to lend, can’t lend fast enough to fill in this gap.

The result is slower growth and a longer path to success for these companies. All because the age-old system of discountable bills of exchange is gone.